| BUDGET 2018/19 – BUDGET SPEECH |

Budget Speech Highlights

Minister of Finance

Malusi Gigaba

21 February 2018

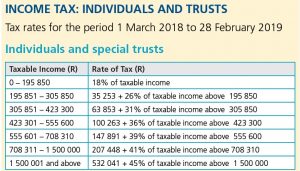

1. Personal income tax relief

The revised tax scales mean:

- The income tax threshold is raised from R75,750 to 78,150 (for persons below 65 years).

- The tax threshold for taxpayers between the age 65 and 74 is increased from R117,300 to R121,000.

- The tax threshold for taxpayers 75 and above is increased from R131,150 to R135,300.

- A maximum tax rate of 45% still applies to income in excess of R1,500,000 (unchanged from 2018).

- The primary rebate is increased to R14,067 (2018: R13,635) for taxpayers under the age of 65 and the secondary rebate for taxpayers over the age of 65 increases to R7,713 (2018: R7,479).

- A third rebate, which applies to taxpayers 75 years and older, increases to R2,574 (2018: R2,493)

2. Increase of interest and dividend income exemption

The domestic interest and dividend income exemption will remain unchanged at R23,800 for taxpayers under the age of 65 and R34,500 for taxpayers aged 65 and over.

3. Motor vehicle allowances

Motor vehicle allowances were reviewed as follows:

Travel allowances:

As per previous year, the actual distance travelled during a tax year and the distance travelled for business purposes substantiated by a log book are used to determine the costs which may be claimed against a travelling allowance.

The maximum value at which the expense schedule is capped remains at R595,000.

80% of the traveling allowance is subject to PAYE.

The percentage is reduced to if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes (unchanged from 2018).

Company cars:

The deemed value (cash cost including VAT) of a company car remains at 3.5% per month.

Where the vehicle is the subject of a maintenance plan at the time that the employer acquired the vehicle the taxable value is 3.25% of the determined value (unchanged).

80% of the fringe benefit must be included in the employee’s remuneration for the purposes of calculating PAYE. The percentage is reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes.

Re-imbursement of travel expenses:

The rate by which travel expenses are re-imbursed has increased to R3.61 per kilometer (2018: R3.55 per kilometer) regardless of the value of the vehicle for distance travelled for business purposes not exceeding 12,000 kilometers.

4. Individual monetary thresholds

· Donations Tax: The annual exemption will remain at R100,000 of property donated for individuals. Donations tax increases from 20% to 25% on donations of more than R30 million.

· Estate Duty: Estate duty exemption will remain at R3,5 million. Estate duty rate increases from 20% to 25% on the dutiable amount of estates of more than R30 million.

5. Capital Gains Tax

- · The inclusion rate for individuals remain at 40%, with the maximum effective CGT rate remaining 18%

- · The annual exclusion for individuals remains at R40,000.

- · The primary residence exclusion remains at R2,000,000.

- · The exclusion on death remains at R300,000.

6. Medical Schemes taxation

Monthly tax credits will be:

- · R310 (2018: R303) – for the first two beneficiaries

- · R209 (2018: R204) – for each additional beneficiary

Where medical scheme contributions in excess of four times the total allowable tax credits plus out-of-pocket medical expenses combined exceed 7.5% of taxable income, they can be claimed as a deduction against taxable income.

7. Other administrative reforms

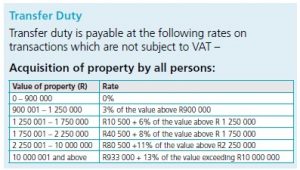

Transfer duties

The value at which property is taxed at 0% remains at R900,000. The maximum rate for properties above R10,000,000 remains at 13%.

- Indirect tax proposals

Value Added Tax (VAT)

The rate of Value added tax increases from 14% to 15% effective 1 April 2018.

The compulsory VAT registration threshold remains at R1,000,000.

Duties on beverages and tobacco products

- · Increase excise duties on alcoholic and tobacco products beverages by between 6% (2018: 6.1) and 10 (2018: 9.5) per cent.

- · Spirits goes up by R4.80 (2018: R4.43) per bottle.

Taxes on fuel

- · The General Fuel Levy has increased by 22 c/l as follows:

- – Petrol increased with 22 c/l to 337 c/l (2018: 315 c/l).

- – Diesel increased with 22 c/l to 322 c/l (2018: 300 c/l).

- · The Road Accident Fund Levy will increase with 30 c/l from R1.63 to R1.93 per liter.

This proposal for Fuel levy changes will take effect from 4 April 2018.

9. Income tax on Companies and Capital Gains Tax on Companies

- · Tax rate for companies will remain at 28%.

- · The tax rate for trusts remains at 45%.

- · The maximum effective Capital Gains tax rate remains at 22.4%.

- · The inclusion rate for Capital Gains Tax for companies remains at 80%.

10. Dividend Withholding Tax

- · The Dividend withholding tax rate remains at 20% for all shareholders receiving dividends.

Other

Carbon Tax

The Carbon Tax Bill is planned to be implemented/effective 1 January 2019.

Cabinet adopted the Carbon Tax Bill in August 2017. Parliament has convened hearings following the release of the draft bill in December 2017. The bill is expected to be enacted before the end of 2018. Government proposes to implement the tax from 1 January 2019 to meet its nationally determined contribution under the 2015 Paris Agreement of the United Nations Framework Convention on Climate Change.

Tax on sugar-sweetened beverages

The new health promotion levy on sugary beverages will be effective 1 April 2018.